Oracle Industry Solutions—Financial Services

The Engaged Financial Services Provider: Meeting Today’s Customer Expectations

A guide to building enduring customer relationships through technology.

You ain’t seen nothing yet.

The financial services industry has seen major changes over the last decade. And the realities, probabilities, and possibilities that lie ahead are unprecedented. It’s going to be an exciting trip—often at seemingly lightning speed—and the question is, what do financial businesses need to do to stay on it for the long haul? One thing is for sure, they’ll need to take care of the people who buy their products and services.

Today’s customers, from across many generations and wealth levels, are hyperconnected. Digital has become mainstream. Customers are doing their financial transactions on digital channels, using their phone. Banks, insurers, investment companies—financial service providers in general—are having to connect with their customers across all financial stages throughout their lives, from saving for and buying their first home to financing a business to planning their retirement.

As more regulations are introduced, these different stages of engagement must be personalised in a way that focuses on an individual customer’s financial best interests. Customers are also looking for the same experiences from their financial providers that they get from digital leaders in other sectors, such as retail, where they can transact from their mobile device and easily move between digital and in-branch discussions with their advisor.

Advisors are looking for the same capabilities in the business environment and want access through mobile and tablet devices with simple point/swipe actions. This will move them from behind the computer to face-to-face interactions with their clients.

In today’s digital era, investors judge investment providers not just against their financial peers, but against technology leaders like Google, Apple, and Amazon.

Becoming engaged, long-term.

Engaged financial services providers must connect with and nurture their customers in the channels of their choice, and in a relevant, fast, and secure way.

In this third of three digibooks, we consider what it means to become an engaged financial services provider, and discuss how they can keep up with today’s consumer expectations and use technology to offer superior customer and employee experiences.

1. What’s Driving Change?

Three key trends.

Digital transformation in the financial sector is allowing providers to increase profitability, productivity, and market share. A loyal banking customer will come to their trusted advisor first to have all of their financial needs addressed. If financial institutions are to compete effectively, they need to keep up with the pace of change while being aware of three key trends that are driving this transformation.

Trend 1: Customer experience.

Customers know what they want, and they want it now.

In today’s digital world, customer expectations have risen considerably, particularly in the retail space. Now, in the financial sector, customers want a more convenient, engaging, and secure user experience.

Executives report fast-rising customer expectations in many areas, from product simplicity/transparency (49%) and anytime, anywhere, any-device access (45%) to robust cybersecurity (43%), more innovative products (32%), and reduced fees (27%).

Digital natives are already doing business via Facebook and other channels that they use all day and every day. WeChat is a giant social media service with more than 900 million monthly active users. In July 2017, it launched WeChat Pay as a mobile payment option for Chinese tourists visiting Europe. And there are many more examples that demonstrate how the bond between social interactions and money grows ever stronger, as customers become more comfortable within their channel.

A button in WhatsApp could wind up being your bank’s most important touch point.Eyal Lifshitz, CEO BlueVine

“Banks and Fintech in 2025: An Unlikely Alliance,” TechCrunch.com, 19 April, 2016

The IDC FutureScape report, “Worldwide Financial Services 2018 Predictions,” states that in 2019 we’ll see peer-to-peer transactions (P2P) worth a total of $6.0 trillion made worldwide using mobile devices.

Consumers are increasingly comfortable with using their mobile devices as tools to manage financial services, including making payments at the point of sale and with friends and family (P2P payments).IDC FutureScape: “Worldwide Financial Services 2018 Predictions”

Trend 2: Rise of fintech.

Look out—fintechs are stealing the show.

For traditional financial services providers, competition from early fintech adopters is strong. Less regulated, and unburdened by legacy IT and physical infrastructure, fintechs have the agility to quickly launch new mobile services that attract customers away from providers that can’t move as swiftly. Fintech is clearly driving the new business model.

Goldman Sachs estimates that fintech startups could steal up to $4.7 trillion in annual banking revenue, and $470 billion in profit, from established financial services companies.

But banks and other financial institutions are seeking to achieve the same level of agility the fintechs have accomplished today. Traditional financial institutions are investing in and collaborating with fintechs by integrating fintech technologies into their own business models to give customers the customer experience they expect.

Trend 3: Security and compliance.

Protect, detect, recover, and comply.

As financial companies embrace the many possibilities of innovative technology, the rapidly increasing number of services and channels has inevitably meant rising cybercrime and greater risk of data breaches. This will challenge security and compliance for the foreseeable future.

$2.1bn is the estimated cost of breaches in 2019 globally.

Financial businesses must develop the capability to meet a constant flow of new or evolving regulations. They must keep financial data secure and comply with in-country data residency regulations. Financial interactions must be tracked and meet compliance rules for acting in the best interests of the customer.

However, digital technology also offers automated compliance solutions—while digital leaders are developing systems that not only detect and protect against security incidents, but also have the resilience to recover quickly from breaches and disruptions.

Responding to regulatory pressure, midsize and community banks will begin to look more at cloud-based compliance analytics platforms and data solutions to improve aspects of their compliance programs, particularly those around KYC (know your customer), CDD (customer due diligence), and AML (anti–money laundering).IDC FutureScape: “Worldwide Financial Services 2018 Predictions”

By looking at just these three key trends—and there are many more—it’s clear that the financial industry is facing irreversible change at a rapid pace. The businesses within it must act now to secure their digital futures and reap the rewards of transformation.

The digitisation of the investment industry is happening. If you are not yet on board, you can expect to start losing business as you’re unable to meet customers’ ever-changing online needs.

“Wealth and Asset Management 2022: The Path to Digital Leadership,” Roubini ThoughtLab

2. The Engaged Provider

Engaging, proactive, fast, and secure.

An engaged provider must strive to do three key things:

- Proactively engage

- Create intelligent interactions

- Be fast, secure, and compliant

Proactively engage

Meeting and nurturing the customer in their channel of choice.

The channel of choice isn’t always going to be owned by the financial provider who is trying to engage a customer. But the engaged provider will use this preferred channel to detect a customer’s needs and provide guidance by meeting them earlier in the purchasing cycle.

For example, a customer can signal that they may be looking to buy a property by searching for houses on sites such as Homes.com or Zoopla.co.uk. They may also be having conversations on social media about their house search—or any other major purchase they may be considering, such as a new car. But they may not necessarily be having a direct conversation with their bank, or mortgage lender or loan companies. So these financial providers must learn from social listening and turn the insights they’ve gathered into meaningful, relevant engagement with their current and potential customers.

MoneyFarm, one of the largest digital wealth management companies in Europe, wanted to build its brand and customer base. Part of its strategy was to automate its marketing processes to improve customer communications. It replaced traditional personalisation techniques with a more streamlined process to better support its marketing team. By carefully managing the introduction of an intelligent automation solution, it ensured customer trust was not impacted.

This online investment advisor implemented Oracle Data Management Platform across search and display channels to help identify site visitors more accurately. Data on visitor digital body language was collected from third-party data, consolidated from websites and social media. This enabled the team to identify the needs of a customer or prospect more accurately for more personalised conversations.

Oracle has enabled us to create more personalised, timely communication campaigns which have already resulted in 30 percent increase in investments.

Create intelligent interactions

Converting data into actionable insights.

Customer intelligence will be the most important predictor of revenue growth and profitability. Financial services institutions have a wealth of historical data about their customers but find it difficult to convert it into actionable insights. They are now investing in machine learning and adaptive intelligence to become more predictive, and to drive their interactions with their customers. They are also using data analytics and visualisation to make sense of that data and deliver value from it.

The businesses that get ahead will be those financial providers that can assemble a 360-degree view of their customer through an aggregated view of household and business, web browsing and social activity. They combine that rich understanding with knowledge of what millions of other similar customers have purchased. This will allow them to anticipate the needs of the customer, engage them in their preferred channel (social, mobile, web, and branch), and provide recommendations that are personalised, yet backed by the learnings from other consumer profiles.

New technologies such as virtual assistants and chatbots will enable financial businesses to respond to customers’ demand for engagement at any time on any channel. And provide relevant information through automated intelligent virtual assistants. This will help free up advisors to provide personal contact when it’s really needed.

Be fast, secure, and compliant

Investing in an agile, secure cloud platform with automated compliance.

Cybersecurity threats and regulatory compliance changes will continue to increase for the foreseeable future. Complex legacy systems are costly and slow to keep up with the pace of change. They consume precious budget and resources that could be better used for innovation.

Financial services providers should ideally be looking to invest in a cloud platform for its agility, and capacity to keep up with the pace of change, as well as its built-in security. Breaches put clients at risk, as well as the hard-earned reputation of the financial provider in question.

We’ve always believed that if we don’t have strong cybersecurity, we’re not going to have a digital business long-term. While we are focused on speed and agility, it can’t be at the expense of safety and security of the data we’re capturing; otherwise, we’ll cut off our nose to spite our face.

“Wealth and Asset Management 2022: The Path to Digital Leadership,” Roubini ThoughtLab

Digital technology is providing new solutions for complying with the ever-growing regulatory burden. Providers should automate compliance as much as possible by building it into all of their systems as they modernise and upgrade. Digital leaders are going beyond this. They’re making it a priority to develop resilient systems that can recover quickly from breaches and disruptions.

A large multinational bank with more than 10 million customers recently used Oracle Customer Experience (CX) to address due-diligence compliance. They modeled 5,000-plus rules in less than three months, and updates to those rules are made in days—not weeks or months. This transparent compliance has saved millions of dollars in auditing costs.

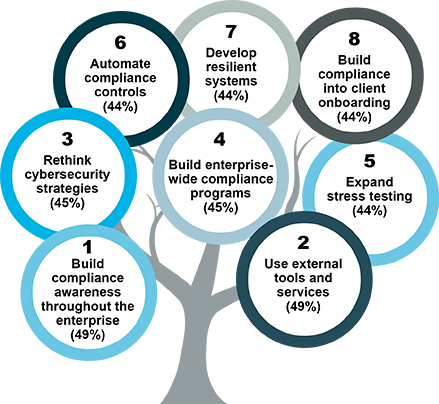

Steps firms are taking to respond to regulatory change using technology.

—“Wealth and Asset Management 2022: The Path to Digital Leadership,” Roubini ThoughtLab