Experience economy

A new customer segment has emerged. These customers, who will be dominant in the 21st century, were born digital and approach their relationships with financial service providers in very different ways. Their loyalty is predicated largely on their satisfaction with digital experiences. They want and expect personalized services from their banks. And they are constantly surveying the wider market for the types of services and experiences they want when their bank doesn’t provide them.

The firms that address this shift by joining data with intelligence at scale are writing the rules for banking in the experience economy—they recognize how they can benefit from process automation, advanced analytics, and an ability to augment the human capacity to take advantage of it all.

“Companies that lead in customer experience outperform laggards by nearly 80 percent.5”

Forbes, 2019

Cyber security

While competing for insights to grow is essential, banks are also competing for insights to protect the bank from harm. New digitally-native criminals are more sophisticated than ever, and banks find themselves under ceaseless cyber attacks—while defending themselves from illicit activities surrounding drugs, human trafficking, and terrorism. Banks that lack modern intelligence are getting hit with higher churn, massive fines, lower valuations, damage to their reputations, and a loss of public trust.

Challenger banks

Today, two out of three new deposit accounts opened online are with direct, non-traditional, cloud-based banks.7 These challengers are more effective at managing customer profiles and anticipating preferences and spending patterns than incumbent banks. And they’re able to acquire and serve customers without building expensive branch networks. By establishing trust through seamless, cross-channel experiences, these new entrants have discovered the recipe—and the technologies—for eroding the incumbents’ customer bases and profit margins.

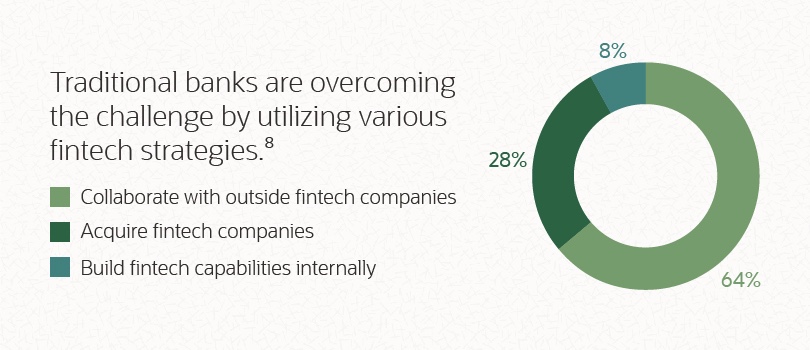

Fintech disruption

In less than 10 years, the financial technology (fintech) phenomenon has split into two main variants—one of challengers that are positioned as an existential threat to incumbent banks, and another as a pool of innovation and collaboration. This has driven the expansion of a relatively smaller set of independent software vendors (ISV) that has serviced the banks for decades, into a US$200 billion fintech supply chain where banks are the keystone species that aggressively help to develop and exploit innovative startups in order to compete against the challengers.

Big tech ambition

Fintech startups are no longer the biggest threat to the industry—but they were the avant-garde. The Big Four, also known as GAFA (Google, Apple, Facebook and Amazon), are the latest challengers. They have dramtically ramped up efforts to offer financial services with strategies to test the market and the status quo. They are also partnering with banks—sometimes big name brands, and other times small and often dormant banks—where they can leverage their native cloud platforms and behavioral customer data. This enables them to offer lower-cost payments, lending, deposit taking, and investment services to their expansive customer sets.

Technology acceleration

With the exponential increase in available data and the widespread adoption of new technologies to query, process, analyze, visualize, and extract business insight from that data, a new world of opportunity is emerging. The impact across the bank’s operations is vast and unrelenting. Whether it’s the war for talent, the ability to build and join new ecosystems, speeding time to market for new products, or reducing the cost of running the bank—these new approaches to managing and leveraging all this data are proven to be critical to the bank’s success.

The debate about the bank’s baseline technology platform has come to rest too—it’s no longer a matter of if, but when, a given computing need will be completely or substantively remade in the cloud. The evidence for this is that after over a decade of tech vendors driving the discussion, banks now find themselves feverishly demonstrating to their stakeholders—and especially regulators—the risks and benefits of moving to the cloud. It’s become clear to them that to compete, they need to move to a lower cost, more flexible, and more extensible technology platform.

“Half the employees working at native cloud competitors are focused on technology, while only 20 percent of employees of incumbent banks can say the same.10”

Why act now?

For years, you’ve been hearing about many of these forces of change. You’ve also been told that the change will only continue to accelerate. And while that’s still true, the difference now is that the rate of change in the market is faster than banks’ ability to evolve. Time is not on their side.

As younger, tech-savvy consumers come to populate the market, the results of disintermediation are becoming apparent. Some banks are selling off business units to remain viable. Others are being acquired. A number of leading banks are restructuring around their core competencies. And with each passing month, banks risk crossing a point of no return where their gradual—and then rapid—decline appears assured.

But it’s not just increased competition that’s causing the decline. Traditional banks struggle to discern clear signals from their existing customers, and can’t see the opportunities for efficiency and growth inherent in their data. Yet both of these are the inputs they need to generate new value.

We see the effects of this changing landscape taking an especially large toll on smaller, community, and regional banks. But even multinational banks are feeling the pressure.

How will your bank survive the extinction-level event? It’s got to adapt.

Learn more about the products that can help. Download the white paper.