AML Program Guide

Why modernize your AML program

As money laundering schemes continue to proliferate, it’s crucial that financial institutions examine their anti–money laundering (AML) compliance guides and strengthen their compliance management programs to defend against bad actors. These crimes can take an immeasurable toll on communities, damaging human lives, wildlife, and the environment, and regulators are increasingly penalizing organizations for noncompliant AML programs. Given the current environment, chief compliance officers (CCOs) must upgrade their program’s effectiveness and efficiency, and now is the perfect time to embark on a journey toward AML program modernization.

A guide to modern anti–money laundering programs

Upgrading compliance management processes with innovative methods is critical to thwarting financial crime. This ebook looks at how AML program modernization can help financial institutions bolster customer satisfaction and optimize ROI.

The AML landscape: rocky and risky

AML programs wrestle with several challenges. For example, transaction monitoring solutions can lack logic and flexibility, resulting in a large number of false positive reports. Moreover, disparate systems and isolated datasets can limit transparency and cause operators to lose valuable time when attempting to rapidly respond to indicators of illicit activity. Banks can eliminate these types of challenges by making sure compliance management protocols and technologies stay up to date. This will help reduce the possibility of compliance costs, suboptimal outcomes, and elevated risk across the AML compliance process.

Current Challenges Across Stages of the AML Program

| Group | Business | AM/Analytics | AML Operations | Financial Investigative Unit | AML Operations | |

|---|---|---|---|---|---|---|

| AML Program Stage | Customer Onboarding | AML Transaction Monitoring | Case Management | Investigation | Regulatory Reporting | Management Reporting |

| High false positives, due to outdated tools and models | High false positives, due to outdated tools and models | Labor-intensive due to high volume of false positive | Manual data collection due to data in multiple systems | Manual creation of reports | Manual creation of reports | |

| Incomplete data/Lack of holistic entity view | Incomplete data/Lack of holistic entity view | Large case workload | No holistic entity view, due to lack of single source of information and lack of visualization tools | Lack of integration with case management | Data in multiple systems | |

| Data in multiple systems | Data in multiple systems | Large backlog | Manual case narratives | Expensive | Lack of intuitive tools | |

| Lengthy onboarding | Incomplete monitoring coverage | N/A | Inefficient | N/A | N/A | |

| Poor customer experience | Inefficient and expensive model simulation | N/A | Expensive | N/A | N/A | |

| Lack of common data model | Lack of common data model | Lack of common data model | Lack of common data model | Lack of common data model | Lack of common data model | |

| Lack of scalability | Lack of scalability | Lack of scalability | Lack of scalability | Lack of scalability | Lack of scalability | |

The impact of relying on legacy systems

Disparate legacy AML systems can pose a real risk to financial institutions because they

- Can’t adjust to ever-changing regulations—legacy systems are rules-based and rely on historical data that doesn’t account for the changing landscape

- Need extensive maintenance and require banks to deploy new point-solution tools and technologies, which must then be integrated into their legacy systems—a process that increases costs

- Reduce efficiency due to the need to intervene with false positives

- Increase financial, regulatory, and reputational risk

- Contribute to customer dissatisfaction caused by false positive alerts

The false positive paradox

False positives, which can account for more than 80% or 90% of alerts, present a prominent challenge to AML programs. Banks must allocate time, manual effort, and budget to thoroughly investigate every false positive. This can spark customer frustration as transactions can be unnecessarily halted. Financial institutions can unlock the true power of automation and tap into efficiencies by reducing the false positive rate.

Modernize today for brighter days ahead

Progressive banks understand their AML compliance guides should no longer be restricted to the risk department but embraced across the entire organization. They are also taking advantage of machine learning technologies. A modern AML mindset means that compliance is no longer thought of as a mandatory exercise but rather a process that can help an organization secure its future. Financial institutions that prioritize AML program modernization can reap extensive benefits, including the following:

- Increased protections for customers, the business, and the financial system because of AML effectiveness

- Greater AML program efficiencies, which enable banks to optimize the impact of resources dedicated to compliance management programs

- Long-term adherence to ever-changing compliance guidelines

- Vast support for CCOs and business growth by improving the accuracy of AML programs, establishing a better Know Your Customer (KYC) experience to improve customer satisfaction, and compiling customer insights that are beneficial to departments across the organization

- An accelerated enterprise data strategy designed to reduce data provisioning time and costs while increasing the quality of service

Increase efficiency and effectiveness with modern AML solutions

With the right set of software solutions, banks can boost the accuracy and efficiency of their financial crime investigations. Learn more about how Oracle’s AML solutions can help minimize risk and provide seamless customer service.

Anatomy of a modern AML program

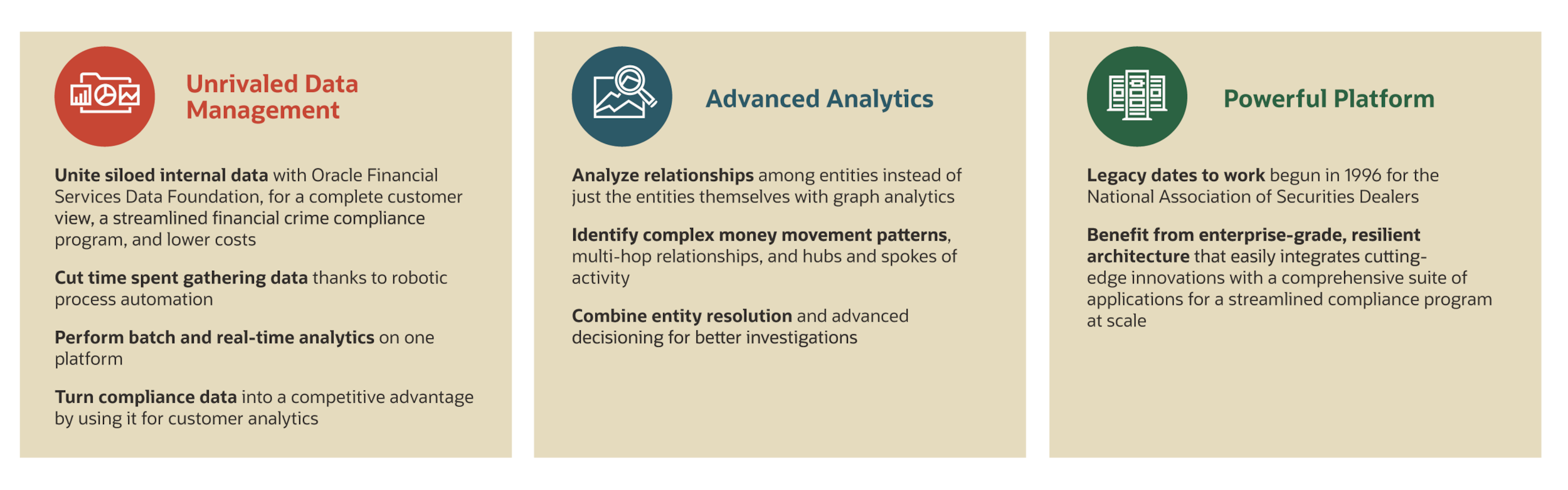

A consolidated back end: When modernizing an AML program, banks must first combine back-end systems to create a single platform equipped to handle KYC/customer due diligence, monitoring, detection, investigation, and reporting. Using a unified platform provides a wealth of benefits and helps AML investigators make accurate decisions by facilitating a holistic analysis of events. Furthermore, it provides cost-saving opportunities by reducing the training required to keep staff up to date on various systems. Lastly, unified platforms can help CCOs visualize compliance operations from end to end and manage operations using a single dashboard.

Unified and context-appropriate data: Modern AML programs require a common data foundation capable of receiving information from any type of data source, including third-party data feeds and fragmented data. This creates a way to compile unified and context-appropriate data, which helps develop consistent, transparent, and auditable operations. Additionally, this modern method of data collection allows organizations to source data only once and use it for other initiatives, instead of repeatedly performing extensive ETL cycles for various business units. Most importantly, unified data helps financial institutions identify new criminal patterns and engineer advanced analytics applications that can improve monitoring, detection, and investigation results.

Advanced analytics: Banks can tap into a variety of advanced analytics solutions at the pace that best works for their organization. Advanced analytics innovations to consider when modernizing an AML program include the following:

- Machine learning to improve detection: Legacy rules-based AML solutions are unable to keep pace with the constant evolution of modern financial crimes, and therefore pose a risk to banks and their reputations. In contrast, machine learning models can rapidly adapt to changing patterns. This innovation doesn’t have to replace rules-based solutions immediately. Machine learning can be run in parallel, giving operators the flexibility to turn off the rules when their regulators feel comfortable. Machine learning models can also help simplify tuning by eliminating the need to tune multiple parameters to achieve a single probability score.

- Graph analytics for better investigations: Investigating highly organized financial crime requires detailed technologies capable of detecting intricate money movement patterns, multihop relationships, and hubs and spokes of activity. Graph analytics (PDF) does just that by leveraging a single source of data, giving investigators the ability to sift through customer information from various points of origin to gain a holistic view of the case. Additionally, this technology can help automatically pinpoint linkages, even if customer information is stored in different silos. When combined with machine learning, graph analytics can correlate suspicious events from disparate systems into a single case. This reduces the compliance management team’s workload as investigators can focus on the whole case rather than single events.

- Entity resolution for a 360-degree view: Graph analytics can also provide entity resolution capabilities to help banks identify different instances of the same entity across data sources.

- Deep learning to find patterns: Previous instances of financial crime can be used to help banks predict new cases of suspicious activity. Therefore, many financial institutions apply deep learning to plot new graphs that are similar to identified criminal patterns. Deep learning is particularly helpful in this instance as it helps investigators evaluate holistic patterns and networks.

- NLP for automatic case narratives: Natural language processing (NLP) expedites investigations by automatically drafting case narratives based on graph visualizations. Additionally, this technology helps reduce human error.

- Collective intelligence and collective learning for recommendations: With knowledge learned from previous case decisions, artificial intelligence can be trained to suggest next steps to investigators. This tool can help new analysts quickly learn how to identify patterns of criminal behavior.

Operational considerations

When updating AML compliance guides, banks will experience positive operational changes. For example, managers can more easily train staff members when the institution uses a single system, and a common data foundation creates a quicker way to share information. Other operational improvements to consider include the following:

- Leveraging open source technologies: Advanced analytics require a suite of digital tools best suited to the needs of staff members. Not only do open source data science languages, technologies, and standards reduce the need to retrain employees, but these innovations can also help increase productivity.

- Operating on the cloud: Modern regulators broadly accept the cloud for AML programs—and for good reason. Operating on the cloud provides significant cost savings by reducing the amount of maintenance required for data center upkeep, offers scalability on demand, and simplifies the upgrade process.

Engineered for success: Oracle Financial Crime and Compliance Management Cloud Service

In the face of ever-changing compliance regulations and rapidly evolving financial criminals, Oracle Financial Crime and Compliance Management helps institutions detect, investigate, and report suspected financial crimes. This solution leverages automated, comprehensive, and consistent surveillance to monitor various parties across all business lines. Furthermore, machine learning technologies, including graph analytics and NLP, strengthen organizational accuracy and efficiencies.